Universal Corporation Stock: Tobacco Demand Remains Strong (NYSE: UVV)

lamyai

In July 2022, we published an article on Universal Corporation (NYSE: UVV), titled: “Universal Corp. could be an attractive buy for dividend investors.” In this article, we looked at several factors that indicated that the actions of the tobacco supplier might turn be a winner in the current macroeconomic environment. We concluded our analysis with a “buy” rating, for the following reasons:

- The stock has historically performed well, in times of low consumer confidence

- The company has a strong track record of paying a safe and sustainable quarterly dividend

- The company seemed to be correctly valued according to Gordon’s growth model.

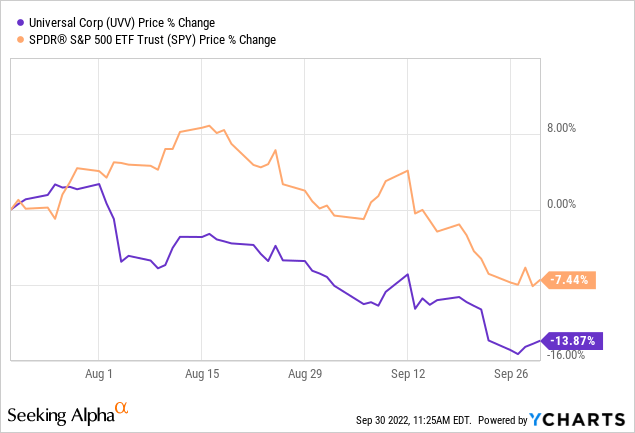

Since we last wrote, UVV’s stock price has fallen significantly.

Today we will provide an updated view on UVV, taking into account the latest earnings reports and macroeconomic developments.

Second quarter results

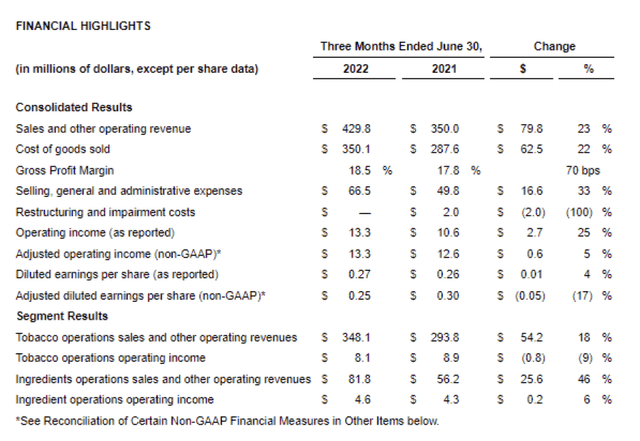

The macroeconomic environment remains difficult, not only for UVV, but for most companies. High raw material prices and transportation costs combined with supply chain constraints are often the main drivers of cost increases. UVV was no exception in the second quarter.

[…] we continued to effectively manage rising costs, particularly rising green leaf tobacco prices and shipping constraints.

Despite these ongoing challenges, the business performed relatively well during the quarter.

Financial Highlights (UVV)

Demand for leaf tobacco remained strong, and flue cured, burley, oriental and wrapper tobacco continued to be undersupplied during the second quarter.

Consolidated revenues increased by $79.8 million to $429.8 million for the quarter ended June 30, 2022, compared to the corresponding period of fiscal 2022, due to higher volumes and prices of carryover tobacco sales as well as the addition of Shank’s in October 2021 in the Ingredients Operations Sector.

In the current market environment, we prefer to invest in companies that sell goods and services, which have inelastic demand. UVV is one such company, as demand for their products remains high despite extremely low levels of consumer confidence.

Additionally, the company predicts that the market is likely to be even tighter for African burley tobacco, as extreme weather conditions have significantly affected the size of crops in Africa during the year. The unfavorable foreign exchange environment and the aforementioned macroeconomic headwinds, however, led to a slight decline in the operating result of the tobacco operations segment.

Tobacco segment results were significantly lower due to unfavorable currency comparisons due to the strength of the US dollar during the quarter ended June 30, 2022. […] Selling, general and administrative expenses for the Tobacco segment increased during the quarter ended June 30, 2022 compared to June 30, 2021, mainly due to unfavorable foreign currency comparisons.

In contrast, the ingredient operations segment is experiencing growth in both sales and operating income. This growth was driven primarily by strong volumes in the human and pet food categories.

Sales from all of our businesses in this segment increased in the quarter ended June 30, 2022, compared to the quarter ended June 30, 2021, with continued strong volumes for the human and pet food categories. Selling, general and administrative expenses for this segment increased during the three months ended June 30, 2022, compared to the same quarter last year, due to the addition of Shank and higher labor costs. -work. […] Ingredients Operations segment revenue of $81.8 million for the three months ended June 30, 2022 increased $25.6 million from the three months ended June 30, 2021, largely due to the addition of Shank’s revenues as well as higher sales volumes and prices.

The positive effects were partly offset by higher raw material prices and higher transportation costs. The company, however, is making progress in creating synergies on the plant-based ingredient platform, which could positively impact the company’s financial statements in the future.

Our companies work together on the development of new products and new strategies to serve the platform’s diverse customers who use our portfolio of plant-based ingredients and botanical extract and flavor offerings.

We believe the company remains attractive as it delivered strong financial results in the second quarter, despite macroeconomic challenges. However, in our view, currency headwinds, high commodity prices and rising transportation costs are likely to continue to negatively impact the company’s financial performance for the foreseeable future.

Based on fundamentals, we believe the selloff since our last write is not warranted. In our view, the firm remains attractive and current price levels could serve as an attractive entry point.

Dividend

In our previous article, we highlighted Universal Corporation’s safe and sustainable dividend payments as one of the main reasons to invest in UVV’s business.

The company recently announced a quarterly dividend of $0.79 per share, in line with the previous quarterly payout. This translates to a return of approximately 6.7% on an annual basis.

As the company continues to pay quarterly dividends, despite macroeconomic challenges and its investment in acquisitions, we believe the company also remains attractive from a dividend investing perspective.

Key points to remember

Universal Corporation posted strong financial performance in the second quarter, fueled by strong demand and pricing.

However, macroeconomic headwinds, particularly high commodity prices, high transportation costs and unfavorable currency environment, continue to negatively impact the company’s financial performance.

The company remains attractive from both a valuation and dividend perspective.

For these reasons, we are maintaining our “buy” rating.